Howard Marks is co-chairman and co-founder of Oaktree Capital Management, an investment manager with more than $120 billion in assets under management. How smart is Marks and how sound is his judgement? Charlie Munger once said: “I probably know Howard Marks as well as I know anybody and he is a very smart man….[For example] you have to believe in the tooth fairy to believe [Bernie Madoff] was having those figures by the methods he claimed to be using. You wouldn’t have gotten that one by Howard Marks for two seconds. I mean you wouldn’t have finished your sentence before he noticed it couldn’t be true. But people don’t think like Howard Marks.”

Marks said in a recent Barry Ritholtz podcast that he believes: “Recognizing and dealing with risk and understanding where we are in the cycle are really the two keys to success.” In a masterful review of Mastering the Market Cycle, Jason Zweig writes:

Mr. Marks admits his book is a kind of tug of war between his certainty that “we don’t know what the future holds” and his belief that “we can identify where the market stands in its cycle.” By studying how the economy, the markets and the psychology of investors all move in long cycles of expansion and contraction, Mr. Marks and Oaktree have been better able to cut back risk near market peaks and ramp it up near market bottoms, he says. But Mr. Marks doesn’t think you can use that sort of understanding to go all in or all out of markets again and again. He likes the book’s subtitle—“Getting the Odds on Your Side”—better than its title, he quips. “Recent performance doesn’t tell us anything we can rely on about the short-term future,” he says, “but it does tell us something about the longer-term probabilities or tendencies.”

It is worth reading what Zweig wrote above is his review of the book at least twice since it represents the core message of Mastering the Market Cycle.

Marks explains in his new book that by doing things like reading widely, studying history and paying close attention to the state of the world right now, an investor or business person can be generally aware of where the cycle might be even though they can’t predict precisely when it will shift in the short term. By doing this work an investor or business person can increase their margin of safety by “getting the odds on their side.” Marks believes that the right way make this analysis is to think probabilistically.” Marks suggested in an interview with Zweig that investors calibrate their exposure to risk using: “a continuum from 0 to 100, he says, with 0 being completely out of the market and 100 being completely in using aggressive techniques like investing with borrowed money.” Having said that, Marks is very wary of attempts to quantify probability given risk, uncertainty and ignorance. He writes in his latest memo:

“while they may not know what lies ahead, investors can enhance their likelihood of success if they base their actions on a sense for where the market stands in its cycle….there is no single reliable gauge that one can look to for an indication of whether market participants’ behavior at a point in time is prudent or imprudent. All we can do is assemble anecdotal evidence and try to draw the correct inferences from it.”

Making this determination requires judgment and there are no recipes for success. An investor has a lot of information about the past and the present, but by definition has zero information about the future. Marks describes this tension by writing in his latest memo: “While the details of market cycles (such as their timing, amplitude and speed of fluctuations) differ from one to the next, as do their particular causes and effects, there are certain themes that prove relevant in cycle after cycle.” Given this reality, how does an investor or anyone making a decision in life “get the odds on their side”? One of the most important themes of Mastering the Market Cycle is reflected in a quote attributed to Mark Twain: “History doesn’t repeat itself, but it often rhymes.” Marks believes that if you read widely and pay attention to what is happening in the world by reading and doing the right research is it possible to see patterns that can inform an investor about the current state of the cycle. Charlie Munger is quoted as saying in a blurb for the new book: “There’s no better teacher than history in determining the future.’ Howard’s book tells us how to learn from history . . . and thus get a better idea of what the future holds.” The words “better idea” are critically important part of that Munger quote are since the objective is find opportunities that reflect favorable odds since decision making certainty is simply not possible to achieve. What Marks is saying is that having the same degree of conviction about all of opinions is dangerous. In an excellent podcast interview with Tim Ferriss, Marks pointed out that: “Nobody ever says, “My opinion is X, and I think I’m wrong.” We all think that our opinions are correct.” It is one thing to have an opinion, but quite another to believe that it is necessarily right.” Marks believes in the value of humility in relation to the markets as he notes here:

There are two things I would never say when referring to the market: “get out” and “it’s time.” I’m not that smart, and I’m never that sure. The media like to hear people say “get in” or “get out,” but most of the time the correct action is somewhere in between. Investing is not black or white, in or out, risky or safe. The key word is “calibrate.” The amount you have invested, your allocation of capital among the various possibilities, and the riskiness of the things you own all should be calibrated along a continuum that runs from aggressive to defensive.

Tim Ferriss just recently posted a fantastic podcast with Mark on this web site in which Howard Marks gives this answer:

One of those most important things is knowing where we stand in the cycle. I don’t believe in forecasts. We always say, “We never know where we’re going, but we sure as hell ought to know where we are.” I can’t tell you what’s going to happen tomorrow, but I should be able to assess the current environment, and that’s the kind of thinking that helped us prepare for the crisis. I think that the two most important things are where we stand in the cycle and the broad subject of risk, and in fact, where we stand in the cycle is the primary determinant of risk.

What Getting the Odds on Your Side means is that we don’t know what’s going to happen – nobody can tell you – but there are times when the outlook for the future is better and there are times when it’s worse, and it’s largely determined by where we stand in the cycle. When we are low in the cycle – that is to say, we’re coming off a bust – the economy is starting to warm up. Investors are just barely starting to switch from pessimism to optimism and prices are starting to rise. Clearly, the odds are in your favor. The outlook is better. It doesn’t mean you’re going to make money, but the chances are good.

On the other hand, when the upcycle has gone on for a long time, when valuations are high, when optimism is rampant, when everybody thinks everything’s going to get better forever, when the economy has been moving ahead for 10 years and it looks like it’s never going to stop, then usually, the enthusiasm has carried the prices to such a high level that the odds are against you. Just knowing that is a huge advantage in investing. You should know that when we’re low in the upcycle, that’s a time to be aggressive, put a lot of money to work, and buy more aggressive things, and when the cycle has gone on for a long time and we’re elevated, that’s the time to take some money off the table and behave more cautiously.”

The link to this Tim Ferriss interview of Howard Marks is in the End Notes to this blog post as is usual. I highly recommend reading the podcast transcript or listening to it. I did both. Twice.

Why economies cycle between better and worse performance is something Marks has thought about a lot. In Mastering the Market Cycle he writes: “The themes that provide warning signals in every boom/bust are the general ones: that excessive optimism is a dangerous thing; that risk aversion is an essential ingredient for the market to be safe; and that overly generous capital markets ultimately lead to unwise financing, and thus to danger for participants.” Marks quotes a Warren Buffett on this point: “The less the prudence with which others conduct their affairs, the greater the prudence with which we must conduct our own.”

What Marks say about the cause of the great financial crisis is a great illustration of what he writes about in this new book. Starting in 2005 and 2006 Marks and his partner Bruce Karsh started to see deals get done on terms that were a “piece of crap.” That investors were buying the offerings anyway made the two partners conclude that something was wrong. Marks admits:

… you can prepare; you can’t predict. The thing that caused the bubble to burst was the insubstantiality of mortgage-backed securities, especially subprime. If you read the memos, you won’t find a word about it. We didn’t predict that. We didn’t even know about it. It was occurring in an odd corner of the securities market. Most of us didn’t know about it, but it is what brought the house down and we had no idea. But we were prepared because we simply knew that we were on dangerous ground, and that required cautious preparation.

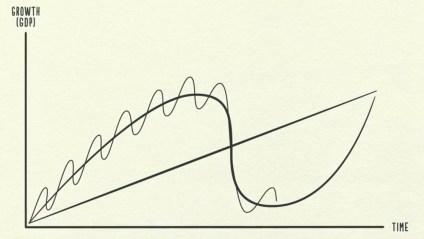

This graphic below appears on page 216 of the new book. It is a graphic representation of why Marks believes that there is value in knowing roughly where the cycle might be even if you can make short term forecasts about where it is going. Marks explains:

“Since market cycles vary from one to the next in terms of amplitude, pace and duration of their fluctuations, they’re not regular enough to enable us to be sure what’ll happen next on the basis of what has gone on before. Thus from a given point in the cycle, the market is capable of moving in any directions, up flat or down. But that does not mean that all tree are equally likely. Where we stand influences the tendencies or probabilities, even if it does not determine future developments with certainty…. Assessing our cycle position doesn’t tell is what will happen next, just what’s more or less likely. But that’s a lot. “

Marks is not the only person who thinks in terms of cycles. Ray Dalio, who writes a very favorable blurb for the new Marks book, believes: “In the business cycle, [a recession] that happens when capacity is constrained and inflation is accelerating and tightness of monetary policy … the long term debt cycle I think is pretty stretched.” One of the cycle charts Dalio uses is:

In his first book The Most Important Thing (which had sale to date of more than 750,000 copies) Marks wrote:

“Cycles will rise and fall, things will come and go, and our environment will change in ways beyond our control. Thus we must recognize, accept, cope and respond. Isn’t that the essence of investing?” “Processes in fields like history and economics involve people, and when people are involved, the results are variable and cyclical. The main reason for this, I think, is that people are emotional and inconsistent, not steady and clinical. Objective factors do play a large part in cycles, of course – factors such as quantitative relationships, world events, environmental changes, technological developments and corporate decisions. But it’s the application of psychology to these things that causes investors to overreact or underreact, and thus determines the amplitude of the cyclical fluctuations.” “Investor psychology can cause a security to be priced just about anywhere in the short run, regardless of its fundamentals.” “In January 2000, Yahoo sold at $237. In April 2001 it was $11. Anyone who argues that the market was right both times has his or her head in the clouds; it has to have been wrong on at least one of those occasions. But that doesn’t mean many investors were able to detect and act on the market’s error.” “A high-quality asset can constitute a good or bad buy, and a low-quality asset can constitute a good or bad buy. The tendency to mistake objective merit for investment opportunity, and the failure to distinguish between good assets and good buys, gets most investors into trouble.” “It has been demonstrated time and time again that no asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheaply enough.”

Marks doesn’t believe anyone should have the same degree of conviction about all of their opinions. To combat a tendency to think in binary terms he advocates that people calibrate risk. Marks recommends thinking about the future as a probability distribution. As an aside, Marks has said he first encountered probability distributions at a World’s Fair in Flushing New York just as I did at the Seattle World’s Fair. In each case there was an exhibit at the fair that dropped balls from the top of a box with regular spaced pegs pegs in it and the resulting cascade produced a bell curve distribution as in the picture below.

What the display at the fair did not teach us is that often the distribution is not a bell curve and that these cases can be extraordinarily important. People like Mandelbrot and Taleb would arrive later and help us understand their impact. Charlie Munger describes what can go wrong:

What they did was, they said, ‘Well, financial outcomes in securities markets must be plottable on a normal curve,’ – [a] so-called Gaussian curve, named for probably the greatest mathematician that ever lived. Gauss must be turning over his grave now with what’s happening. Of course, the math was very helpful because you could come up with numbers and results that would make people feel confident with what they were doing. There was only one trouble with the math: The assumption was wrong. Financial outcomes in securities markets are not plottable. It is not a law of God that outcomes in securities prices will fall over time on a curve and [follow] reality according to Gauss’s curve. Quite the contrary, the tails are way fatter…. People were actually making decisions about how much risk to take, based on the application of correct math, based on an assumption that wasn’t true. And by the way, people gradually knew it wasn’t true.”

Marks tells a great story about one situation when he and his partner were worried about buying distressed asset after the great financial crisis. They eventually decided to keep buying assets and distressed prices since if the prices did not recover nothing really mattered financially anyway. This presented a situation with a huge potential upside and a very small down side from the investments (optionality). On the subject of today’s markets, Marks believes that the baseball inning analogy he has used several times is not a good one since there is no set number of innings when it comes to the cycle. His most current statement on valuation is:

“equities are priced high but (other than a few specific groups, such as technology and social media) not extremely high – especially relative to other asset classes – and are unlikely to be the principal source of trouble for the financial markets…. Oaktree’s mantra recently has been, and continues to be, “move forward, but with caution.” The outlook is not so bad, and asset prices are not so high, that one should be in cash or near-cash. The penalty in terms of likely opportunity cost is just too great to justify being out of the markets.”

One of my favorite parts of the Tim Ferriss podcast is when Marks makes a point that has been a consistent theme of this blog: “there are many ways to invest; there are many people who engage in activities that I think can’t be done, and there are many people in each one who do very well. I don’t say mine is the only way. Venture is an example.” Marks agrees with Charlie Munger on the importance of “the discipline of mastering the best that other people have ever figured out. I don’t believe in just sitting down and trying to dream it all up yourself. Nobody’s that smart.” During a lunch with Marks Munger once said: “It’s not supposed to be easy. Anyone who finds it easy is stupid. There are many layers to this, and you just have to think well.” But it can get easier if you work hard and stay humble by recognizing what you do not know. As Michael Mauboussin likes to say: “the best long-term performers in any probabilistic field — such as investing, sports-team management, and pari-mutuel betting — all emphasize process over outcome.”

Speaking of probabilistic bets, Marks believes that the best games for improving decision-making involve uncertainty and ignorance. Annie Duke explains:

Trouble follows when we treat life decisions as if they were chess decisions. Chess contains no hidden information and very little luck. The pieces are all there for both players to see. Pieces can’t randomly appear or disappear from the board or get moved from one position to another by chance. No one rolls dice after which, if the roll goes against you, your bishop is taken off the board. If you lose at a game of chess, it must be because there were better moves that you didn’t make or didn’t see. You can theoretically go back and figure out exactly where you made mistakes.

Marks meets with Munger now and then and I wish he would write a post about Charlie. Marks describes what makes Munger so interesting and effective as an investor as follows:

“The main thing is that he has read more broadly. He’s had another 22 years to read further, and he was probably always a broader reader than I was, and so it’s his ability to call on these references. In a way, it’s kind of silly to think that we can reinvent all the wisdom in the world. It’s great to borrow from others, and Charlie does that broadly, and I try to do it, but he just knows more.”

Marks has over 100 memos on his web site. And he says: “The price is right, since it is free.” When asked by Barry Ritholtz why he writes, Marks responded:

“For ten years I never had a response [to my memos]. Not only did nobody say they thought they were good, nobody even said that they got it. The interesting question is: What kept me going? I have no idea. The answer I think is that I was writing for myself. Number one, it is creative and I enjoy the writing process. Number two, I thought that the topics were interesting. Number three, writing helps you tighten up your thinking.”

My motivation in writing over a million words on this 25IQ blog is the same. I would be writing even if no one was reading.

End Notes:

Mastering the Market Cycle: https://www.amazon.com/Mastering-Market-Cycle-Getting-Odds/dp/1328479250

The Most Important Thing: https://www.amazon.com/Most-Important-Thing-Illuminated-Thoughtful/dp/0231162847/ref=pd_lpo_sbs_14_img_2?_encoding=UTF8&psc=1&refRID=SG7YP40QCQ398D52DR2G

Memos from Howard Marks: https://www.oaktreecapital.com/insights/howard-marks-memos

Zweig Article on Marks: https://www.wsj.com/articles/you-can-time-the-market-just-not-all-the-time-1536922831

Tim Ferriss Podcast: https://tim.blog/2018/09/25/howard-marks/

Ritholtz podcasts:

https://ritholtz.com/2017/02/howard-marks-books/

https://ritholtz.com/2017/02/mib-howard-marks-matters/

Dalio on cycles: : https://www.marketplace.org/2018/09/20/world/dalio-debt-cycle and https://www.youtube.com/watch?v=PHe0bXAIuk0

My blog post: A Dozen Things I’ve Learned About Investing from Howard Marks (July 30, 2013) https://25iq.com/2013/07/30/a-dozen-things-ive-learned-about-investing-from-howard-marks/

My blog post: A Dozen Ways to Apply the Lessons Taught in the Book “The Most Important Thing” (September 17, 2016). https://25iq.com/2016/09/17/a-dozen-ways-to-apply-the-lessons-taught-in-the-book-the-most-important-thing-by-howard-marks/