Asking me to select my favorite book written by Michael Mauboussin is like asking me to pick my favorite child. I love them all the same. But if I had to choose one book it would probably be The Success Equation. There are lot of reviews of this book, all of them glowingly positive. The world doesn’t need another review of this great book so I will try to write mostly about how the ideas in the book might be applied in the real world.

Anyone who has been reading this blog should know a lot about Michael Mauboussin. He is one of the clearest business thinkers ever in my view. When he writes and speaks it is in complete thoughts to an extent that astounds me. Read his books and essays. Then read them again. He is a wonderful teacher and very generous with his ideas and time.

It is rare that a post on this blog does not have a notes section identifying further resources to read, but this one is particularly long since Mauboussin’s written work is voluminous. He is a reading and writing machine.

One of the many things I like about Mauboussin is that he thinks about thinking. That is not only valuable, but fun. I am lucky to count him as a friend. His ideas have shaped mine about as much as anyone. Let’s get started.

1. “There’s a quick and easy way to test whether an activity involves skill: ask whether you can lose on purpose. In games of skill, it’s clear that you can lose intentionally, but when playing roulette or the lottery you can’t lose on purpose.” Luck is easier to describe than skill. Luck is best thought of in terms of an activity like roulette. With roulette you know the all potential future states and the probability distribution. Because the house takes a rake in roulette, there are no professional roulette players. Very few things in life involve just luck. The probability distribution of outcomes in the real world is rarely known. Mauboussin writes that luck has three core elements: 1) it operates on an individual or an organizational basis; 2) it can be positive or negative; and 3) it is reasonable to expect that a different outcome could have occurred.

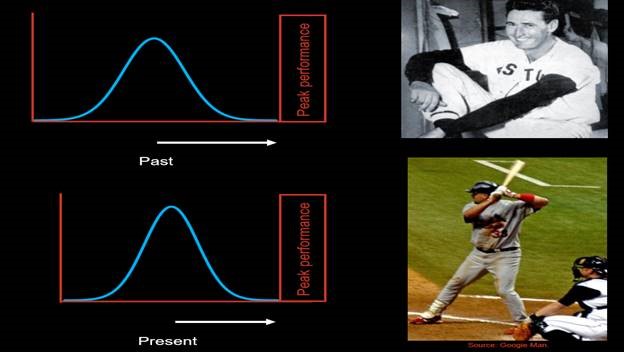

Skill is harder to define, but Mauboussin believes a dictionary definition works well. Skill is: “The ability to apply one’s knowledge readily in execution or performance.” Mauboussin writes that activities like chess rely almost wholly on a player’s skill. Mauboussin explains that each sport has a different mix of skill versus luck and if you want to understand this point better read the book! You will note that in this picture below investing finds its home closer to luck than skill (see the placement of chart icon).

2. “Much of what we experience in life results from a combination of skill and luck.” The mix between skill and luck in a given business or investing activity is always different and is constantly changing. Exactly where investing falls on that continuum depends on the style of investing involved and the business environment at the time. Investing in the stock market is an interesting case to consider when thinking about the mix between luck and skill since it is hard to do better than an index and it is also hard to do worse, especially if you are diversified. Venture capital investing is a more a skill driven activity since it involves things like coaching founders and significantly more uncertainty. Starting a business also involves more skill than investing in pubic equities. When Mauboussin was writing The Success Equation we had an email conversation about the role of luck in the success of Microsoft. I recall that we did not agree completely about the mix in that case. I recall that saw less luck that Mauboussin did. But I am too close to the story perhaps to be objective. Mauboussin includes writes in the book: “When asked how much of his success he would attribute to luck, Gates allowed that it played ‘an immense role.’ In particular, Microsoft was launched at an ideal time: ‘Our timing in setting up the first software company aimed at personal computers was essential to our success,’ he noted. ‘The timing wasn’t entirely luck, but without great luck it wouldn’t have happened.’

3. “Great success combines skill with a lot of luck. You can’t get there by relying on either skill or luck alone. You need both.” Sometimes you will hear people say things like: “the harder I work, the luckier I become.” Mauboussin easily demonstrates these statements to be a non sequitur with a few well-chosen words: “there is no way to improve your luck, because anything you do to improve a result can reasonably be considered skill.” This Mauboussin turn of phrase reminds me a lot of the classic Howard Marks line: if risky investments could be counted on to deliver high returns, then they wouldn’t be risky.

4. “So here’s the distinction between activities in which luck plays a small role and activities in which luck plays a large role: when luck has little influence, a good process will always have a good outcome. When a measure of luck is involved, a good process will have a good outcome but only over time.” Mauboussin believes a wise investing process has three elements: 1) you must find something the market does not believe and you must be right about that belief; 2) you must have control over your behavioral biases; and 3) you must not have organization issues that get in the way of a sound decisions. One way to find things that are true that the market does not believe is to find areas of the market that are less well known and popular. In other words, what you want to do is find a game where the competition is weak. This is exactly what investors Warren Buffett and Howard Marks recommend. What you want to do is find a bet where the other bettors are making decisions based on things that are the equivalent of the patterns made by sheep guts at a slaughterhouse or a Keynesian Beauty Contest. Munger says: “For a security to be mispriced, someone else must be a damn fool. It may be bad for the world, but not bad for Berkshire.” Warren Buffett makes the point that the way to beat a chess master is to play them at something other than chess. Buffett adds: “The important thing is to keep playing, to play against weak opponents and to play for big stakes.” If you’ve been playing poker for half an hour and you still don’t know who the patsy is, you’re the patsy.”

There is no substitute for a sound process in an activity like investing. Mauboussin writes:

“If you compete in a field where luck plays a role, you should focus more on the process of how you make decisions and rely less on the short-term outcomes. The reason is that luck breaks the direct link between skill and results—you can be skillful and have a poor outcome and unskillful and have a good outcome. Think of playing blackjack at a casino. Basic strategy says that you should stand— not ask for a hit—if you are dealt a 17. That’s the proper process, and ensures that you’ll do the best over the long haul. But if you ask for a hit and the dealer flips a 4, you’ll have won the hand despite a poor process. The point is that the outcome didn’t reveal the skill of the player, only the process did. So focus on process.”

5. “When everyone in business, sports, and investing copies the best practices of others, luck plays a greater role in how well they do.” “It’s not that investors lack skill. As investors have become more sophisticated and the dissemination of information has gotten cheaper and quicker over time, the variation in skill has narrowed, and luck has become more important.” Mauboussin calls this idea the paradox of skill. For example, as the skill levels of portfolio managers rise the greater the role of luck becomes in the outcome. The classic example of this idea that Mauboussin cites is the .400 batting average of Ted Williams. One of the many joys of this book is how easily he conveys ideas that involve statistics. Mauboussin points out: “The average of all batting averages in Major League Baseball is generally in the range of .260 to .270. In 1941, when Williams achieved his feat, the standard deviation was .032. Today it is about .028. Saying this differently, Ted Williams had an average that was 4 standard deviations away from the average, getting him to .406. If a player were to be 4 standard deviations away from average in 2011, he would have hit .380. Awesome, but nowhere near .400.” Charlie Munger once said, “If you don’t get this elementary, but mildly unnatural, mathematics of elementary probability into your repertoire, then you go through a long life like a one-legged man in an ass-kicking contest. You’re giving a huge advantage to everybody else.”

As investors increasingly move toward buying index funds, unskilled investors are removed from the game which makes the task of a manager trying to earn alpha harder. In their book The Incredible Shrinking Alpha, Larry Swedroe and Andrew Berkin argue that active managers are increasingly competing for a shrinking pool of alpha. So as investment skill levels rise, luck gets more important.

6. “If you take concrete steps toward attempting to measure [the contributions of skill and luck to any success or failure], you will make better decisions than people who think improperly about those issues or who don’t think about them at all. That will give you an enormous advantage over them.” The more data you have on your processes and outcomes the more you will be able to improve those processes and outcomes. What data is valuable? I would rather have data and not need it, than need it and not have it. This quote makes me think of a quality that Mauboussin and I share. We both want to know why something is true. It is not enough to know that x is true. Why is X true? One way to know more about why something is true is to measure it. Of course people tend to ignore or hide data they do not like, which reminds me of an old joke told by Kieran Healy:

A soldier is captured during a long-running war and thrown into the most stereotypical prison cell imaginable. Inside the cell is another solider. He has an enormous, disgusting-smelling beard and has clearly been there a long time. The young solider immediately sets about trying to escape. He is resourceful and possessed of great willpower. He bribes a guard with his emergency supply of cash. The guard gets him into a supply truck and he makes it to the prison garage, but is found during a routine vehicle search while exiting the compound. He is returned to his cell. His mangy companion says nothing about his departure or return. Undeterred, the young soldier works on the bars of the cell for weeks, filing them down with a shim made from a toothbrush. The whole time the old soldier looks on, silently. The young soldier finally breaks the bars, slips out the window and makes it to the outer wall, where he is spotted and recaptured. He is thrown back in the cell. He glowers at his grizzled companion, who still remains silent. Calming himself and mastering his despair, he tries yet again, this time digging a tunnel with the narrow end of a broken plastic coffee spoon. After about two years of work he succeeds in escaping under the wall and making it to the nearest town, only to be captured again at the train station. He is delivered, once again, back to his cell and its taciturn occupant. At the end of his wits, the young soldier finally confronts the old soldier, shouting, “Couldn’t you at least offer to help me with this?! I mean, I’ve come up with all these great plans—you could have joined me in executing them! What’s wrong with you?” The old soldier looks at him and says, “Oh I tried all these methods years ago—bribery, the bars, a tunnel, and a few others besides—none of them work.” The young soldier looks at him, incredulous, and screams “Well if you knew they didn’t work, WHY THE FUCK DIDN’T YOU TELL ME BEFORE I TRIED THEM, YOU BASTARD?!” The old soldier scratches his filthy beard and says, “Hey, who publishes negative results?”

7.“Not everything that matters can be measured, and not everything that can be measured matters.” People want to be able to predict the future. To satisfy that desire, humans have a tendency to grab what data can be measured and assume that what can’t be measured does not exist or does not matter. People who are mathematically gifted are particularly prone to this tendency. For example, if you just assume that the human world works like the world of physics you can use this assumption make beautiful mathematical formulas. But there may or may not be any tie of that mathematics to reality, which can create a host of major problems. As an example, one of my biggest problems with a lot of economic discussions today related to the fact that it is very hard to measure consumer surplus. Just ignoring consumer surplus because you can’t measure it well is a bad idea that can lead to unhelpful policy conclusions. Just as unhelpful are people who say that it can be accurately measured, based on a bunch of assumptions that are essentially guesses. Sometimes we need to accept that we do not or cannot fully know something. The policy choices must deal with that uncertainty.

8. “Even if we acknowledge ahead of time that an event will combine skill and luck in some measure, once we know how things turned out, we have a tendency to forget about luck.” Survivor bias is a huge problem in human cognition. The tendency is for people to conclude: what I achieve is skill and what I fail at is luck. Too often recollections of events we see in life is best categorized as fiction. People love to tell stories, particularly about their successes. Sometimes we get lucky and sometimes we are skillful. Usually the result is some mix of both. Charlie Munger has said on this topic: “Well, some of our success we predicted and some of it was fortuitous. Like most human beings, we took a bow.” What is particularly bothersome to me is when people ascribe luck to themselves in a way that they bestow themselves some moral measure superiority. As Warren Buffett points out, he won the ovarian lottery: “I was born in the United States. I had all kinds of luck.”

9. “One of the main reasons we are poor at untangling skill and luck is that we have a natural tendency to assume that success and failure are caused by skill on the one hand and a lack of skill on the other. But in activities where luck plays a role, such thinking is deeply misguided and leads to faulty conclusions.” One of the aspects of life that bothers me the most is when I encounter someone who attributes all their success to skill, and as a result of that they assign a higher moral standing to themselves than people who have been less successful. Mauboussin illustrates this point with a story:

“For almost two centuries, Spain has hosted an enormously popular Christmas lottery. Based on payout, it is the biggest lottery in the world and nearly all Spaniards play. In the mid-1970s, a man sought a ticket with the last two digits ending in 48. He found a ticket, bought it, and then won the lottery. When asked why he was so intent on finding that number, he replied “I dreamed of the number seven for seven straight nights. And 7 times 7 is 48.”

10. “The trouble is that the performance of a company always depends on both skill and luck, which means that a given strategy will succeed only part of the time. So attributing success to any strategy may be wrong simply because you’re sampling only the winners. The more important question is: How many of the companies that tried that strategy actually succeeded?” Once up a time long ago I read a book called In Search of Excellence. The authors analyzed leading companies are sorted out the secrets of success in a way that suggested that it was a replicable formula. The best companies do X, Y and Z was the claim. What was missing of course were all the companies that did X, Y and Z and failed. Mauboussin writes:

“There are numerous books that purport to guide management toward success. Most of the research in these books follows a common method: find successful businesses, identify the common practices of those businesses, and recommend that the manager imitate them. Perhaps the best known book of this genre is Good to Great by Jim Collins. He analyzed thousands of companies and selected 11 that experienced an improvement from good to great results. He then identified the common attributes that he believed caused those companies to improve and recommended that other companies embrace those attributes. Among the traits were leadership, people, focus, and discipline. While Collins certainly has good intentions, the trouble is that causality is not clear in these examples. Because performance always depends on both skill and luck, a given strategy will succeed only part of the time.

Jerker Denrell, a professor of behavioral science, discusses two crucial ideas for anyone who is serious about assessing strategy. The first is the undersampling of failure. By sampling only past winners, studies of business success fail to answer a critical question: How many of the companies that adopted a particular strategy actually succeeded?”

As an example, I knew someone once who though that since X successful founder yelled at people that he must yell at people to succeed. People do things like see fictional accounts of Facebook in a movie and think that all they need to do is replicate that formula. Hoodies or black turtlenecks are not highly correlated with startup success. If enough people wear hoodies sure one of them will succeed to, but there is no causation involved. Free Kind bars and colorful plastic slides between floors of an office do not cause startups to succeed financially.

11. “The process of social influence and cumulative advantage frequently generates a distribution that is best described by a power law. … One of the key features of distributions that follow a power law is that there are very few large values and lots of small values. As a result, the idea of an “average” has no meaning.” I call this the paradox of luck as a riff on Mauboussin’s “paradox of skill.” My thesis is that the luckier you get, the more skill you can get if the conditions are right. This happens because of what is known as “cumulative advantage.” As an example, the more financial success someone like a venture capitalist gets, the more skilled people they get to work with since they are attracted to that success, which makes the venture capitalist more skilled, which makes them more financially successful [repeat]. My thesis is: financial success caused by luck begets not only greater financial success, but greater skill. A good example on this point is a statement made by Michael Moritz years ago. He said: “I know there are millions of people around the world have worked as hard and diligently as I have and weirdly enough, like [former US President] Jimmy Carter said years and years ago, ‘life’s unfair’. I just happen to have been very fortunate.” “A chimpanzee could have been a successful Silicon Valley venture capitalist in 1986.” The key point about what Moritz describes is that luck did not just make him richer, it made him more skilled since he was exposed to opportunities and teachers that he would not otherwise have encountered. Being lucky made him more skilled and that process fed back on itself. Luck and skill are different but one can lead to the other in a way that create a virtuous circle.

12. “Knowing what you can know and knowing what you can’t know are both essential ingredients of deciding well.” The best investors are certain of just about nothing and spend a lot of time trying to learn more about what they do not know and cannot know. Mauboussin is chairman of the board of trustees of the Santa Fe Institute, a leading center for multi-disciplinary research in complex systems theory. Perhaps the greatest things I have learned about complex adaptive systems is to more aware of what I do not know.

There is a difference between knowing what you do not know and not knowing very the basics necessary to do a job. As an example, I’m of the view that a US President should know what Aleppo is or be able to name a few foreign leaders. And you want you investment managers to understand things like, well, compound interest and capital gains. Call me a stickler on this point if you want. A positive example would be an investor who candidly says, “I don’t understand biotech investments.”

If you ever attend a meeting at Sante Fe Institute meeting you will see famous investors in the audience who are hungry for information on what they do not know or can’t know. Great investors are humble but yet aggressive when they see a significant opportunity within their circle of competence. Munger is a good person to give the closing statement:

“Even bright people are going to have limited, really valuable insights in a very competitive world when they’re fighting against other very bright, hardworking people. And it makes sense to load up on the very few good insights you have instead of pretending to know everything about everything at all times.”

Notes:

The Success Equation (the book): https://www.25iqbooks.com/books/3-the-success-equation-untangling-skill-and-luck-in-business-sports-and-investing

My previous post on Mauboussin on 25IQ: https://25iq.com/2013/07/11/a-dozen-things-ive-learned-from-michael-mauboussin-about-investing/

My list of Mauboussin Essays: https://25iq.com/2013/02/17/mauboussin/

More than You Know: https://www.25iqbooks.com/books/5-more-more-than-you-know-finding-financial-wisdom-in-unconventional-places-updated-and-expanded-columbia-business-school-publishing

Think Twice: https://www.25iqbooks.com/books/4-think-twice-harnessing-the-power-of-counterintuition

Expectations Investing: https://www.25iqbooks.com/books/24-expectations-investing-reading-stock-prices-for-better-returns

Mauboussin’s bio/CV: http://www.santafe.edu/about/people/profile/Michael%20Mauboussin

Mauboussin’s Web site http://www.michaelmauboussin.com/

Fast Company Interview: https://www.fastcompany.com/3002729/facts-luck

CNBC post: http://www.cnbc.com/id/49791755

Strategy-Business: http://www.strategy-business.com/article/13202a?gko=50b64

Bloomberg: https://www.bloomberg.com/view/articles/2016-08-16/michael-mauboussin-on-skill-and-luck

Talk at Google: https://www.youtube.com/watch?v=1JLfqBsX5Lc

Ritholtz MIB Podcast: https://www.bloomberg.com/view/articles/2016-08-16/michael-mauboussin-on-skill-and-luck

Economist: http://www.economist.com/blogs/buttonwood/2012/12/investing

Wharton: http://knowledge.wharton.upenn.edu/article/michael-mauboussin-on-the-success-equation/

Wealth of Common Sense: http://awealthofcommonsense.com/2013/07/do-you-feel-lucky/

Essay on Measuring the Moat: http://csinvesting.org/wp-content/uploads/2013/07/Measuring_the_Moat_July2013.pdf

Essay on the Skill Paradox: http://changethis.com/manifesto/100.03.SuccessEquation/pdf/100.03.SuccessEquation.pdf

Wired Interview: https://www.wired.com/2012/11/luck-and-skill-untangled-qa-with-michael-mauboussin/

Forbes interview: http://www.forbes.com/sites/investor/2013/11/05/the-role-of-luck-and-skill-in-investing/#7368a94e3e4c

Prisoner Joke: http://crookedtimber.org/2011/04/23/i-predict-the-gifted-will-foresee-the-punchline/

- A Dozen Ways You Can Use Seth Klarman’s “Margin of Safety” Approach When Voting

- A Half Dozen Things I’ve Learned from Robert Cialdini’s book “Influence”

Categories: Uncategorized